Why Web3 will accelerate carbon project financing

Why Web3 will accelerate carbon project financing

An explainer of VCM supply-side innovations enabled by blockchain technology

The recent COP 27 conference in Egypt highlighted that public finance will not be enough to reach societal net zero by 2050. Total climate finance was only $632 billion on average for 2019 and 2020,1 while estimates suggest that a net-zero transition will require annual investments of $9.2 trillion in physical assets alone by 2050.2 It is clear we need private investment (lots of it), and the voluntary carbon market (VCM) is an important vehicle to channel these capital flows.

As the need to scale the VCM grows, entrepreneurial teams and large organizations have continued to explore different solutions across the value chain. One promising area - known as regenerative finance (or ReFi) - leverages blockchain technology and innovations from decentralized finance to address a variety of VCM challenges. Since 2021, dozens of ReFi projects have launched and received funding, tackling everything from trading and derivatives to offsetting and data analytics.

But what supply-side challenges does blockchain aim to solve? How does it help accelerate carbon project development and financing now and in the future? And which projects are actively building in this space?

This article is a continuation from a previous post where I introduced a simplified framework for the emerging on-chain carbon market. The key topics surfaced and addressed below continue to be explored market-wide and will evolve over time. My aim here is to share a point-in-time perspective of the challenges and opportunities that exist and discuss how this still nascent technology might be used in the future.

What challenges exist to developing and financing carbon projects?

Carbon project development remains a risky business for developers, investors, and buyers.

1) The lack of a reference price for carbon inhibits price risk management and access to financing

One of the main challenges to scaling the VCM is the absence of a (deeply) liquid reference price for carbon credits.3 Under the current system of carbon procurement, where corporate off-setters still largely access credits through intermediaries (brokers or retailers), market prices and volume information are opaque. Without a trusted price for carbon, developers struggle to estimate return on investment for a potential project, and their negotiating position is subsequently weakened when defining contractual terms with potential buyers and investors. This means that projects are either less likely to secure the required capital, or the terms of the investment are less attractive for the developer. With much of the current profit pool being captured by brokers, retailers and vertically integrated developers, the opportunity of passing more value back to the project developer could make initiating a new carbon project more attractive in the first place.

2) The preference for large-scale project financing disadvantages smaller developers

Developers with smaller carbon credit portfolios may struggle to secure financing from larger intermediaries, trading houses and investment funds. This is because there is an increasingly strong preference for operators with solid track records and large volumes to meet the demand from corporate emitters. According to data from Allied Offsets,4 the current developer ecosystem is highly concentrated, with the top 30 players contributing nearly half of total credit volumes globally. While it is unclear how many projects might not have been funded due to this preference, it is certainly true that we should be making funding as accessible as possible, particularly for high integrity projects creating benefits beyond carbon removal.

3) The terms of payment can sometimes lead to working capital shortfalls for developers

Carbon project developers can sometimes face a working capital deficit during the life of a project, as income is received only when credits are issued by the registry. Prepayments are often used to account for cash flow gaps and manage pricing risk, but this type of agreement is also highly inefficient for the buyer since capital is generally outlaid months before credits are delivered. Given forward contracts are non-standardized agreements entered into bilaterally, buyers will find them difficult to sell or use as a productive asset on the balance sheet. While demand for securing carbon credits is certainly high, an efficient VCM should try to eliminate all frictions that demand-side participants face.

How does the on-chain carbon market address these challenges?

Blockchain offers two main benefits to project development and financing:

A liquid and transparent market provides the foundation to efficiently price (and re-price) carbon project investments and spot or forward credit purchases.

A decentralized governance model and accessible fundraising tools provide project developers the ability to raise capital and originate credits more easily

Note, while some of the points discussed below are predicated on real functionality that exist today, other points are more conceptual / future-oriented.

1) Liquidity and transparency improves market efficiency and enables direct access

Digital carbon assets, exchanges, and marketplaces enable anyone to provide liquidity and execute transactions in real-time and at low cost. The creation of carbon pools - where projects of similar methodologies, vintages and other traits are bundled together - allows for a more efficient matching of buyers and suppliers, and is analogous to the “core carbon reference contracts” discussed by the Taskforce for Scaling the VCM. Through tools like KlimaDAO’s carbon dashboard, the price and volume transparency of the public blockchain then levels the playing field further, enabling all market participants to make decisions with complete and up-to-date information. A liquid and transparent market provides the foundation to efficiently price (and re-price) carbon project investments and spot or forward credit purchases.

For project developers, price and volume information can be used as a basis to estimate project return-on-investment and negotiate financing terms with potential investors. Similarly, developers can use this information to define the price and delivery methods for carbon offtake agreements with buyers and off-setters. With greater clarity on market conditions, developers can negotiate more favorable pricing for forward credits and lower their cost of capital, further incentivizing the creation of more carbon projects in the future.

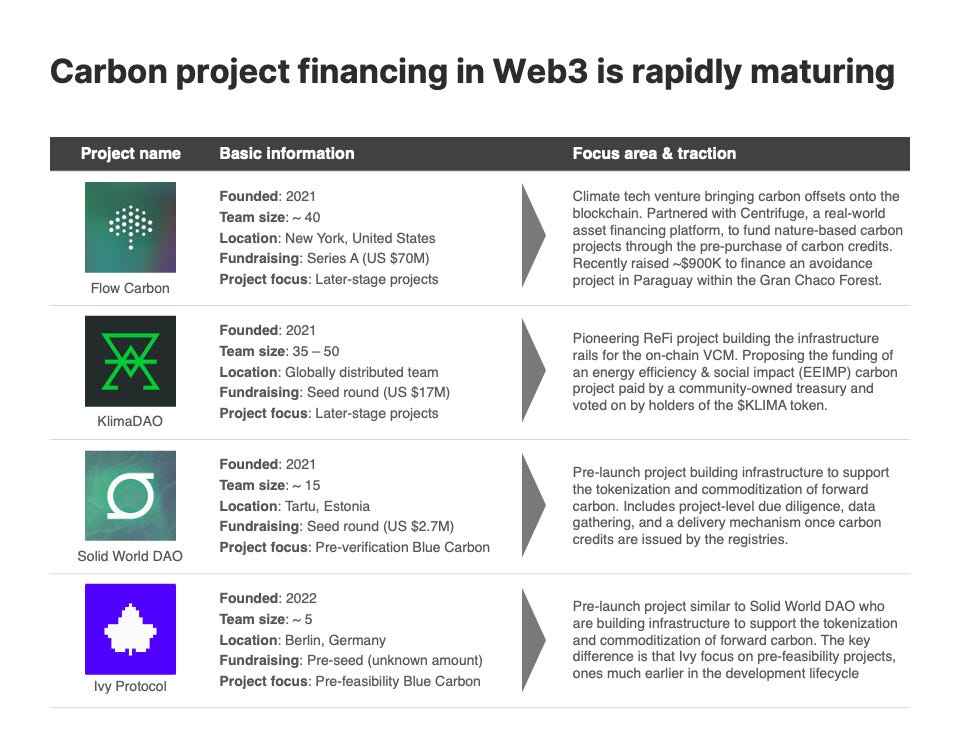

For credit buyers and investors, the same techniques that have worked for ex-post credits can also be applied to forward carbon agreements (or ex-ante credits). This means that by standardizing and tokenizing them, forward agreements can become much easier to buy and sell on the secondary market, decreasing the risk for buyers who would otherwise need to lock their capital up for years. Assuming deep liquidity for forward carbon, buyers might therefore be more willing to provide pre-payment for future delivery, helping to address working capital shortfalls for developers. While still pre-launch, projects like Solid World DAO and Ivy Protocol are building bespoke infrastructure to support the commoditization of forward credits, with their initial focus being specifically on smaller-scale blue carbon projects.

Beyond de-risking early-stage investments, a liquid spot market also gives project developers the opportunity to access the market directly. Rather than needing to sell through a broker or retailer, the permissionless nature of decentralized exchanges and peer-to-peer marketplaces allow credits to be sold easily on the spot market. By making it easier to own the customer relationship directly, project developers will ultimately benefit from higher profit margins compared with selling through an intermediary.

2) Decentralization unlocks new sources of fundraising and streamlines credit origination

Decentralized finance provides the most cost-effective way to pool and distribute capital between large groups of investors.5

If supported by careful project-level due diligence, appropriate legal structures and targeted toward sophisticated investors, early-stage carbon projects could emerge as a compelling “real world asset” (RWA) investment class to a range of investors. As an example, with billions of dollars currently sitting idle in the wallets of thousands of organizations and individuals in Web3, the on-chain economy could soon become a meaningful catalyst for carbon project financing. This would be especially true for smaller projects that are currently underserved by the existing off-chain financial institutions.

Organizations like Flow Carbon and Centrifuge have already operationalized investment vehicles to partly crowdfund the purchase of forward carbon and are intending to explore earlier stage project investments in the future. Other groups like KlimaDAO, following a proposal between C3 and StarCB to create an energy efficiency & social impact (EEIMP) carbon pool, are proposing the funding of an EEIMP-compatible carbon project paid by a community-owned treasury and voted on by holders of the $KLIMA token.

In addition to financing projects, decentralization also offers the ability to streamline the credit origination process itself. Using token-weighted voting and dMRV technology, organizations like Regen Network and Nori are defining digital-native carbon methodologies and working with a range of projects to issue “ecocredits” (a term encompassing traditional carbon credits, as well as credits that focus on biodiversity, agroforestry, and ocean regeneration) and carbon removal credits respectively. While these initiatives are still in their early stages (for reference, as of November 2022, Regen has issued ~180k tCO2e and Nori ~124K tCO2e), the promise of tapping into the long tail of projects is certainly worth exploring.

But why blockchain?

While many of the challenges discussed here could eventually be addressed without the use of blockchain, the unique opportunity of the technology comes down to the speed at which it can solve the various VCM scaling issues.

For the most part, the industry is only about 12 months old. Yet, the impact on the broader VCM has been incredibly rapid.

Just over the past year…

24M+ tCO2e of carbon credits have been bridged and 250K+ tCO2e retired on-chain by hundreds of different organizations and individuals

Each of the largest carbon registries (Verra, Gold Standard, and ACR) have all held public consultations and are actively exploring how blockchain might be used in the future of the VCM.

The World Economic Forum’s Crypto Sustainability Coalition was recently formed to investigate the role of Web3 technologies in fighting climate change

Hundreds of projects have launched, and some have raised capital, each tackling different challenges across the VCM value chain.6

This impact is only made possible by the decentralized, permissionless and interoperable design of blockchains. A decentralized and permissionless design enables the complex ecosystem of VCM participants to work together much more easily than they would be able to without it. The accessibility of data provides a single source of truth for the entire market to base decisions on, improving both supply and demand side issues. A composable and interoperable technology stack accelerates development timelines and increases opportunity for innovation.

On this last point, the founder of Aave puts it well.

While it is certainly possible to build using the Web2 stack, the speed at which we need this market to evolve should push us to embrace Web3. Regardless of how the market evolves, the need to accelerate both the supply and demand of offsets is clear, and there appears to be no sign that the pace of change is slowing.

https://www.climatepolicyinitiative.org/publication/global-landscape-of-climate-finance-2021/

https://www.mckinsey.com/capabilities/sustainability/our-insights/the-net-zero-transition-what-it-would-cost-what-it-could-bring

https://www.iif.com/Portals/1/Files/TSVCM_Report.pdf

https://alliedoffsets.com/

https://www.imf.org/en/Publications/GFSR/Issues/2022/04/19/global-financial-stability-report-april-2022#Chapter-3:-The-Rapid-Growth-of-Fintech:-Vulnerabilities-and-Challenges-for-Financial-Stability

https://kumu.io/climate-collective/web3-climate-map

Fascinating and compelling. In a space with more good actors than bad, a focus on enablement and access feels right and Web3 is great for the long tail.